Covid-19: Pandemic of the 21st Century Part 3: Monetary and Fiscal Policies

Prepared by Mak Yee Than

Monetary Policies: How Did Central Banks Respond?

In the face of major recessions domestically and globally, central banks around the world have rolled out monetary policies of various types and levels of aggressiveness, which primarily seek to ensure adequate liquidity in financial systems to stimulate consumption and growth. The People’s Bank of China was the first to respond, while the Federal Reserve has been by far the most aggressive.

Monetary policy refers to actions taken by a country’s central bank or monetary authority to influence borrowing costs and control money supply, as a way to meet certain macroeconomic objectives such as growth, inflation, employment and price stability. Among the tools of monetary policy are interest-rate cuts, asset purchases, currency interventions and liquidity injections.

In the following section, we will look at the responses and actions taken the central banks of some of the major economies in the world.

1. People’s Bank of China

| Date | Action |

| Feb 1 | Announced multi-agency package to support financial system. |

| Feb 2 | Increased bank liquidity by the size of RMB1.2 trillion {US$174 billion) via large repo operation. |

| Feb 6 | Announced RMB300 billion of special re-lending through national and local commercial banks. |

| Feb 7 | Announced steps to support bond issuance by financial institutions. |

| Feb 16 | Reduced medium term lending facility rate by 10 basis points (bp). |

| Feb 19 | Reduced 1-year loan prime rate by 10bp and 5-year loan prime rate by 5bp. |

| Feb 25 | Increased re-lending and re-discount quota; increased policy bank lending. |

| Mar 1 | Announced temporary deferred repayment of principal and interest on loans to small and medium-sized enterprises. |

| Mar 13 | Reduced bank required reserves by 0.5% to 1%. |

| Apr 3 | Reduced the reserve requirements for smaller banks to release around 400 billion yuan (US$56.3 billion) in liquidity. |

| Apr 7 | Reduced interest rate on banks’ excess deposits from 0.72% to 0.35%. |

| Apr 15 | Conducted a Medium-term Lending Facility (MLF) operation of 100 billion yuan, cutting the MLF rate by 20bps on 15 April. |

| Apr 21 | Conducted a RMB 5 billion Central Bank Bills Swap of 3 months tenor with the rate of 0.10%. |

| Apr 24 | Injected 56.1 billion Yuan into the market via its Targeted Medium-term Lending Facility (TMLF). The facility has a maturity of one year and an interest rate of 2.95%, 20bps lower than 3.15%, the rate of the previous TMLF operation. |

2. Bank of Japan

| Date | Action |

| Mar 13 | Offered unspecified “ample” liquidity for repo market. (Source: https://www.boj.or.jp/en/announcements/release_2020/rel200313c.pdf) |

| Mar 16 | Increased purchases of ETFs at an annual pace of around ¥12 trillion ($112.55 billion), JREITs to ¥180 billion per year, and set aside ¥2 trillion for loans secured by commercial paper and corporate bonds. |

| Mar 24 | Announced additional measures to maintain stability of repo market that consist of extension of the implementation period for increasing the number of government securities issues offered in the securities lending facility and the relaxation of the upper limit on the number of government securities issues allowed for the submission of bids for the securities lending facility. (Source: https://www.boj.or.jp/en/announcements/release_2020/rel200324b.pdf) |

| Apr 27 | Announced enhancement of Monetary Easing: Increased in purchases of CP and corporate bonds; Strengthening of the Special Funds-Supplying Operations to Facilitate Financing; Further active purchases of Japanese government bonds (JGBs) and treasury discount bills (T-Bills). |

3. European Central Bank

| Date | Action |

| Mar 12 | Announced additional long-term refinancing operations (LTROs) for banks, more favourable LTRO terms in upcoming operations, additional asset purchases, temporary capital, and operational relief to banks. |

| Mar 18 | Increased asset purchases by €750 billion through 2020. |

| Mar 19 | Clarified new asset purchases will be flexibly allocated across members. |

| Mar 20 | Reactivated 24 billion Euro swap line with Denish central bank. |

| Mar 25 | Expanded the range of eligible assets under the CSPP to non-financial commercial papers, making all commercial papers of sufficient credit quality eligible for purchase under CSPP. |

| Apr 7 | Adopted a package of temporary collateral easing measures to facilitate the availability of eligible collateral for Eurosystem counterparties to participate in liquidity providing operations. |

| Apr 16 | Announced a temporary reduction in capital requirements for market risk, by allowing banks to adjust the supervisory component of these requirements. |

| Apr 30 | Decided to conduct a new series of seven additional longer-term refinancing operations, called pandemic emergency longer-term refinancing operations. |

4. Bank of England

| Date | Action |

| Mar 11 | Reduced bank rate by 50bp; announced Term Funding Scheme with additional incentives for SMEs; maintained stock of corporate bond and gilts; reduced counter-cyclical capital buffer; communicated supervisory expectation that banks should not increase dividends or other distributions, such as bonuses. |

| Mar 17 | Announced Covid Corporate Financing Facility, which will buy a type of debt called commercial paper with a maturity of up to 12 months from businesses which had an investment-grade credit rating or similar pre-crisis. |

| Mar 19 | Reduced bank rate 15bp; increased asset purchases by £200 billion; enlarged Term Funding Scheme. |

| Mar 24 | Launched Contingent Term Repo Facility, a flexible liquidity insurance tool that allows participants to borrow central bank reserves (cash) in exchange for other, less liquid assets. |

| Mar 30 | Announced that it will continue to offer the Contingent Term Repo Facility (CTRF) on a weekly basis through April 2020. |

| Apr 6 | Announced Term Funding Scheme to open for drawing on 15 April 2020 that allow allows eligible banks and building societies to access four-year funding at rates very close to Bank Rate. |

| Apr 24 | Announced continue to offer 3-month and 1-month term Contingent Term Repo Facility (CTRF) operations on a weekly basis through May 2020. |

| May 2 | Announced a change to the Term Funding Scheme with additional incentives for SMEs. |

| May 7 | Maintained Bank Rate at 0.1% and to continue with the programme of £200 billion of UK government bond and sterling non-financial investment-grade corporate bond purchases. |

5. The Federal Reserve

| Date | Action |

| Mar 3 | Reduced federal funds rate by 50bp (unscheduled). |

| Mar 9 | Increased repo offerings by $75 billion. |

| Mar 11 | Increased repo offerings further to as much as $505 billion. |

| Mar 12 | Extended maturity distribution of Treasury security purchases; increased term repo operations by large amount (more than $1 trillion). |

| Mar 15 | Reduced federal funds rate by 100bp to near zero; announced purchases of $500 billion in longer-term Treasury securities and $200 billion in agency mortgage-backed securities; reduced primary credit (discount window) rate by 150bp to 0.25%; announced miscellaneous other steps to support the flow of credit. |

| Mar 15 | Coordinated central bank action to enhance the provision of global US dollar liquidity. |

| Mar 17 | Urged banks to use capital and liquidity buffers in joint supervisory statement. |

| Mar 17 | Announced Commercial Paper Funding Facility to support the flow of credit to households and businesses. |

| Mar 17 | Announced Primary Dealer Credit Facility which aims to ease recent liquidity strains in the repo market by providing lender-of-last-resort financing for primary dealers. |

| Mar 18 | Announced Money Market Mutual Fund Liquidity Facility to broaden its program of support for the flow of credit to households and businesses. |

| Mar 19 | Established temporary dollar liquidity arrangements with additional central banks. |

| Mar 20 | Coordinated central bank action to further enhance the provision of US dollar liquidity. |

| Mar 20 | Expanded money market mutual fund liquidity facility to make loans secured by certain municipal money market mutual funds. |

| Mar 22 | Provided additional information to encourage financial institutions to work with borrowers affected by COVID-19. |

| Mar 23 | Announced Treasury purchases and agency Mortgage Backed Securities (MBS) in “amounts needed”; included commercial MBS in purchases; announced measures to provide a combined $300 billion in new financing, including $30 billion from the Exchange Stabilization Fund (ESF); established Primary and Secondary Market Corporate Credit Facilities; established Term Asset-Backed Securities Loan Facility enabling asset-backed securities backed by student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration, and certain other assets; expanded Money Market Mutual Fund Liquidity Facility and Commercial Paper Funding Facility. |

| Mar 26 | Working with other financial supervisors, communicated to banks various regulatory actions to encourage lending. |

| Mar 27 | Working with other financial supervisors, communicated to banks various regulatory actions to encourage lending. |

| Mar 31 | Announced the establishment of a temporary repurchase agreement facility for foreign and international monetary authorities (FIMA Repo Facility) to help support the smooth functioning of financial markets. |

| Apr 9 | Taken additional actions to provide up to $2.3 trillion in loans to support the economy. |

| Apr 23 | Announced temporary actions aimed at increasing the availability of intraday credit extended by Federal Reserve Banks on both a collateralized and uncollateralized basis. |

Fiscal Policies: What Stimulus Plans Did The Governments Introduce?

As countries around the world grapple with the economic disruption that resulted from the Covid-19 pandemic, their respective governments had embarked on fiscal stimulus programs to mitigate the macro and micro-economic shocks, such as contraction in GDP, deflation, failing businesses and industries, loss of jobs etc.

To address the problems mentioned, fiscal stimulus is undertaken in the form of government spending and tax policies. Proponents of Keynesian economic theories believe fiscal stimulus is an effective way to mitigate economic recession by influencing aggregate demand, which have been the blueprint for governments and economic policymakers for almost every crisis since the Great Depression.

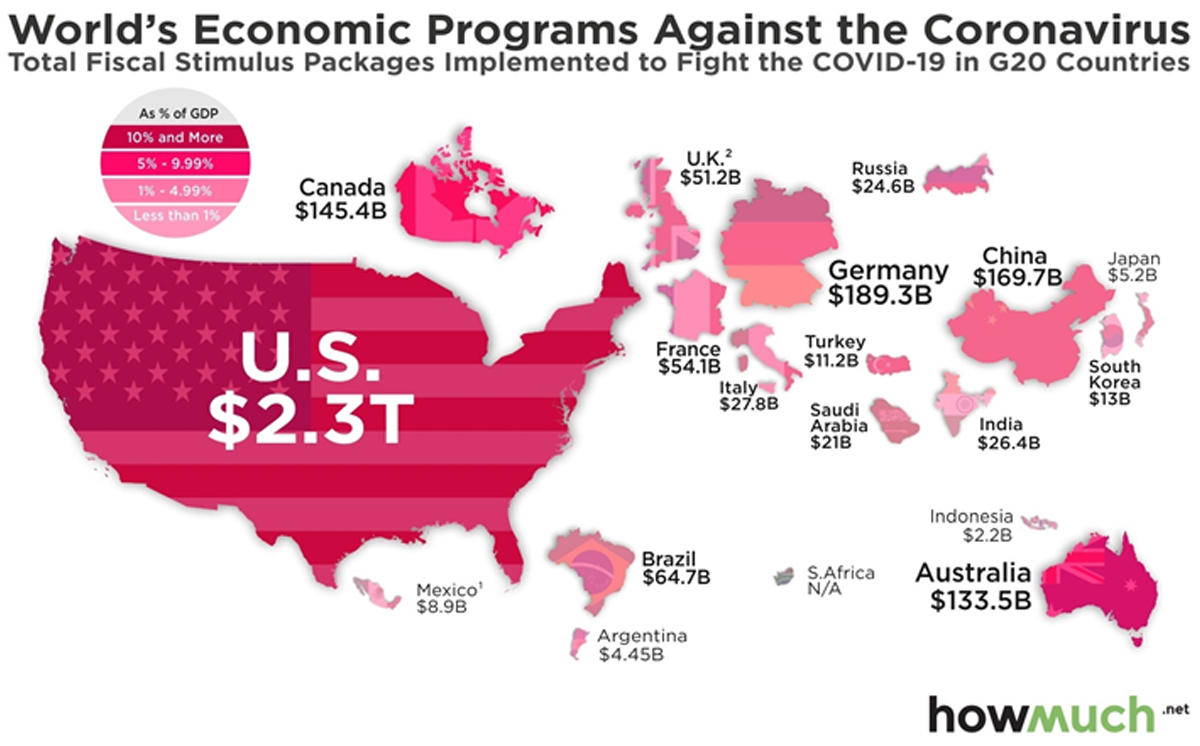

Below is an illustration of the fiscal stimulus packages launched in G20 countries:

Image source: https://howmuch.net/articles/worlds-economic-programs-against-coronavirus

1. China

It was reported on March 19, China plans to release trillions of yuan through fiscal stimulus into the economy, by spurring investment in infrastructure that will be backed by as much as 2.8 trillion yuan of local government special bonds.

On March 27, the ruling Communist Party’s Politburo said it would step up macroeconomic policy changes and pursue more proactive fiscal policy. Measures include an expansion of the budget deficit, increased issuance of local and national bonds, lower interest rates, delayed loan payments, removal of supply chain bottlenecks and greater consumption.

Earlier in the year, the central government announced smaller-scale fiscal measures such as tax breaks, slashed power charges and fee reductions.

As of mid-March 2020, prepaid spending vouchers aimed at boosting consumer spending had been given out by local governments, albeit relatively small amounts. Banks were asked to extend the terms of business loans and appeals were made to commercial landlords to reduce rents. Additional subsidies from provincial and local governments for certain auto purchases, and increased limits on car ownership were introduced. Furthermore, smaller companies were afforded debt deferments, mortgages and other personal loans were given forbearance.

2. Japan

Given their close economic ties and geographical proximity with China, which was the first epicentre of the virus outbreak, Japan was quick to recognise the threat it poses to the economy. As early as February, the first, of three spending bills, was passed as a package of loans for small businesses worth $4.6 billion.

The Japanese government on March 10 announced they would step up fiscal spending by 430.8 billion yen, mostly used to support small and medium-sized businesses affected by the crisis. Other spending includes upgrading medical facilities and subsidies for working parents who have been forced to go on leave to care for their as a result of school closures.

Prime Minister Shinzo Abe on April 7 unveiled an economic stimulus package of unprecedented scale, equivalent to 20 percent of the country’s GDP. The 108 trillion yen package includes 6 trillion yen in cash pay-outs to households and small and medium-sized firms, which are also allowed to borrow at zero interest from private financial institutions.

3. United States

The U.S. government introduced three major fiscal stimulus packages, and one supplemental one, amounting to nearly $2.8 trillion.

The first, known as the Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, was enacted on March 6, 2020. It provided $8.3 billion for vaccine research, financial aid to state and local governments to combat the epidemic, and efforts in fighting the spread of the virus overseas.

The Families First Coronavirus Response Act, which came in little under two weeks after the first package, covered subsidies for families who depend on free school lunches, tax credit for companies that were mandated to provide paid sick leave for employees suffering from Covid-19, roughly $1 billion to states for insurance costs, as well as funding to allow free-for-all Covid-19 testing. The second stimulus package was worth $3.4 billion.

Costing $2.3 trillion, the third stimulus package, known as the Coronavirus Aid, Relief, and Economic Security Act (or CARES Act), was the largest in U.S. history. Elements of the bill include a $500 billion lending program to support distressed companies, a $367 billion fund for small businesses through the Paycheck Protection Program (PPP) and expanded Economic Injury Disaster Loan (EIDL) program, $250 billion in unemployment insurance benefits and direct payments of up to $3,000 to millions of American families, among others. A supplementary package, which added $484 billion to PPP and EIDL, as well as for funding of hospitals and testing, was later signed into law.

4. United Kingdom

In the first of its four stimulus packages on March 11, the U.K. government appropriated nearly $37 billion to provide tax cut for retailers, cash grants for business, subsidy to bear the costs of sick pay for small businesses, and benefits for the self-employed and unemployed.

The second package came at a cost of $379 billion, earmarked for business loans and loan guarantees which were accessible for business of various sizes. Additionally, tax cuts and funding were afforded to businesses worst affected by the pandemic, such as retail and hospitality.

The third and fourth packages included wage subsidy for companies to keep workers employed, tax credits for low-income and unemployed individuals, deferment of the Value Added tax, and cash aid for the self-employed.

5. Germany

A wide range of aggressive fiscal stimulus and relief measures was launched by the Germans, being the largest among European countries in absolute terms and percentage of the national GDP.

The massive €600 billion Economic Stabilization Fund offers $432 billion in loan guarantees, $108 billion to buy equity stakes in struggling companies, and $108 billion to the German Development Bank to refinance loans to businesses.

A supplementary budget, worth €122.5 billion, involves suspending existing government debt rules, to provide €50 billion to small businesses and self-employed individuals, funding for PPE, vaccine research, and other public health expenditure, among others.

Additionally, the government allowed tax deferment or waiver for those adversely affected by the pandemic.

Ending Thought…

The economic fallout resulting from the Covid-19 pandemic is seen by many to be worse than the Great Recession of 2007-2009, and possibly as severe as the Great Depression of 1929-1933. With most of the world still fighting the pandemic and struggling to reopen economies, it remains to be seen if the aggressive and, in some cases, unprecedented monetary and fiscal actions would yield significant and effective results in paving the way for an economic recovery.

At the same time, the urges to provide reliefs and rescues to the economy by implementing excessive economic stimuli that normally associate with loosening of credit control could spur credit and liquidity risk to the financial system.

Lastly, we believe that a more pragmatic approach to the pandemic lies within how agile we are to be adaptive enough to the new normal way of lifestyle, way conducting business, economic condition and investment environment before a safe drug or vaccine can be discovered to treat or prevent the virus.

Thank you !

Thank you for reading & Stay Safe !

Please visit our website : www.www.kenangafutures.com.my for more reading material.

Download full article here

Disclaimer:

This document has been prepared solely for the use of the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without the prior written permission from Kenanga Futures Sdn Bhd. Although care has been taken to ensure the accuracy of the information contained herein, Kenanga Futures Sdn Bhd does not warrant or represent expressly or impliedly as to the accuracy or completeness of the information. This information does not constitute financial or trading advice neither does it make any recommendation regarding product(s) mentioned herein. Kenanga Futures Sdn Bhd does not accept any liability for any trading and financial decisions of the reader or third party on the basis of this information. All applicable laws, rules, and regulations, from local and foreign authorities, must be adhered to when accessing and trading on the respective markets.