KF Spotlight – Brent & WTI Crude – A Well-Oiled Rally?

Prepared by Zainal Aiman

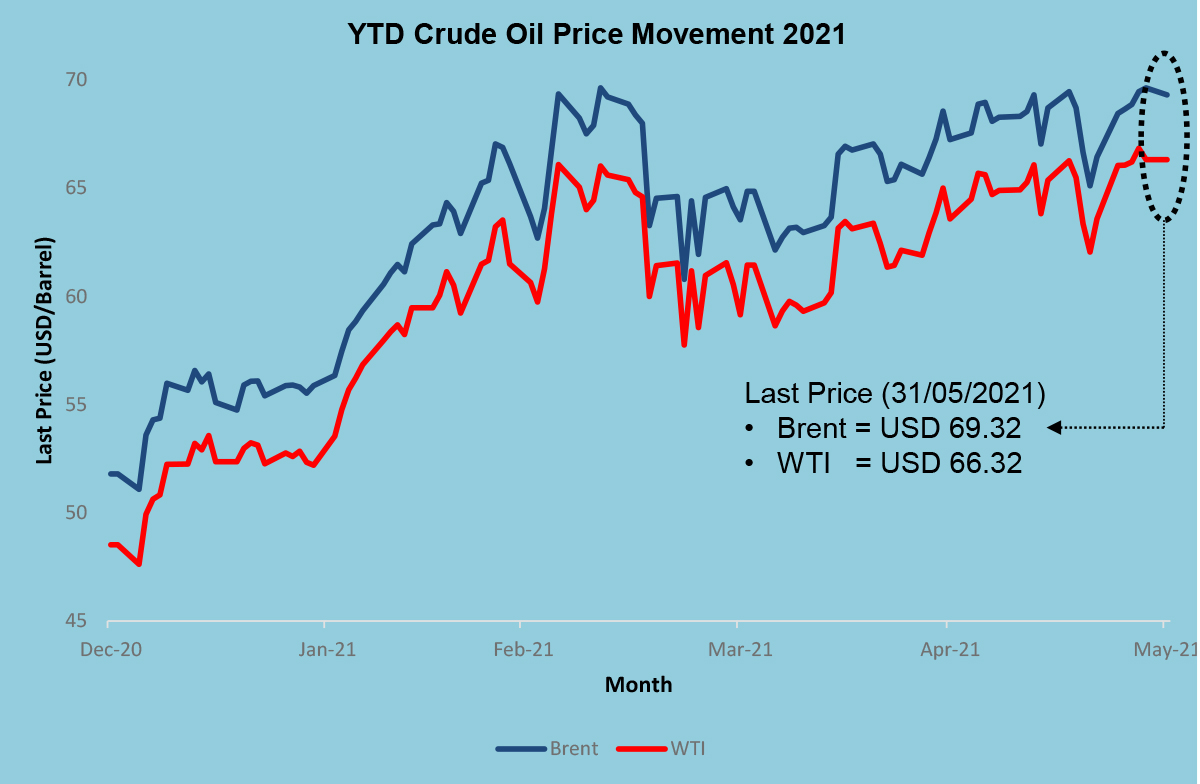

YTD HIGH :

Brent – 69.63 (11/03/2021) WTI – 66.09 (05/03/2021)

YTD LOW :

Brent – 51.09 (04/01/2021) WTI – 47.62 (04/01/2021)

Correlation :

+0.97

Data as at 26 May 2021

Source : Bloomberg

After experiencing a collapse in oil price last year, due to oil price war and Coronavirus pandemic, crude oil market has recovered, mostly driven by the reopening of economies especially from the major countries.

This can be seen from the chart above when both Brent and WTI crude oil bounced higher from their YTD low level of USD 51.09/barrel and USD 47.62/barrel respectively, registered on 4th January 2021, to their YTD high level of 69.36/barrel and 66.09/barrel on 5th March 2021. Prices then seemed to stabilize at a range of USD55 and above.

In this paper, we will examine what factors are driving the rally of crude oil prices in the first quarter of 2021 and what factors that need to be monitored closely for the rest of the year.

YTD-2021 Market Review

Vaccination Program Leads the Rally

Since last quarter of last year, crude oil market began to stage a rally largely driven by a run of positive news related to COVID-19 vaccine effectiveness. The positive sentiment was carried forward into the first two months of 2021, driving some optimism on global oil demand recovery when countries like US and UK approved the use of some vaccines to their population.

Stable Oil Demand Recovery

The steady performance of the crude oil in Q1 2021 can also be attributed to the global oil demand recovery. According to CME Group, global oil demand, which was falling as much as 30% during COVID-19 lockdowns, is now back to about 95% of its pre-pandemic level. The improvement can be attributed to the recovery of industrial production as well as the abnormally low temperatures in some regions during this period.

Supply Restrictions Support the Prices

In the first quarter of 2021, global crude oil production was affected due to several factors. In February 2021, crude oil supply fell to 91.6 million bpd due to a number of attacks on oil production facilities in Saudi Arabia, while a reduction in supply in the US due to record cold weather had also pressured crude supply. In addition, the decision by OPEC+ to maintain production restrictions had also helped to boost the prices.

Source : CNBC, Reuters, EIA, CME Group

Factors to Watch in H2 2021

COVID-19 Uncertainty Likely to Persist

Despite the positive development on the vaccine rollout program in most major countries, the return to normalcy is still distant. The rally in crude oil prices began to slow down in the end of first quarter caused by the threat from the third wave of the pandemic, especially in Europe and India. Furthermore, aviation fuel, which account for most of the crude oil demand factor, has been the hardest-hit segment of oil demand. It remains to be seen how this sector will perform in 2021.

OPEC+ Decision to Increase Production Volumes

Following the OPEC+ meeting on 1st April, it was decided that the crude oil production volume will be increased by 1.15 million bpd from May within a three month timeframe. Meanwhile, Saudi Arabia will gradually ease its voluntary production cut of 1 million bpd and increase its production by 250,000 bpd in May, and 350,000 and 400,000 in June and July respectively. Given the uncertainty in global demand, this decision might provide some pressure on crude oil price rally.

Expectation of Growing US Shale Production

Last year saw the occurrence of oil price war that caused the negative prices in WTI crude oil. US producers responded by reducing capital spending, drilling and jobs which resulted to lost production of about 2 million barrels per day. There is high possibility that US producers would increase their shale supply this year given the prospect of economic recovery where according to EIA, US oil production is anticipated to increase by 1 million barrels.

The Prospect of Weakening in US Dollar

The prospect of stronger US economy in 2021 was driven by a number of supportive programs. US Federal Reserve has announced their intention to keep the interest rates low while, US president Joe Biden has introduced a large stimulus package to boost their economy. An economic recovery is typically a sign for weakness in US dollar, which would be a bullish indicator for oil prices in 2021.

Geopolitical Situation remains unclear

The first quarter of 2021 already saw a geopolitical crisis that caused some disruption to global crude supply when an oil production facilities in Saudi Arabia were attacked. Geopolitical uncertainty is likely to persist in the coming months as Iran, one of the top oil producing countries, is heading into their presidential election where hardliners are hoping to unseat reformists to block any cooperation between US and Iran. Furthermore, under the new US administration, the future of US-China trade relationship also remains uncertain.

Source : Oilworld, EIA, CNBC and API

A Short Term Price Outlook

1) Brent Crude Oil

2) WTI Crude Oil

Source : Bloomberg

A Short Term Price Outlook

Based on the technical chart, prices for both Brent and WTI crude oil had shown a remarkable performance from early November onwards, when MACD bullish crossover was formed. Brent and WTI crude oil had surged 33.90% and 36.21% respectively to reach YTD high level of USD69.36/barrel and USD66.09/barrel on 5th March 2021.

However, a MACD bearish crossover was formed in early May 2021, causing both oil prices to ease from their YTD high. Prices then traded in a range bound movement afterwards.

In the near term, we foresee that both Brent and WTI crude oil would face a strong support level of USD60/barrel and USD55/barrel, respectively. If these levels are broken, the next support level of Brent and WTI are USD55/barrel and USD 45/barrel, respectively. Overall, we expect both Brent and WTI crude oil to trade in a range of USD60/barrel to USD70/barrel.

Download full article here

Disclaimer:

This document has been prepared solely for the use of the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without the prior written permission from Kenanga Futures Sdn Bhd. Although care has been taken to ensure the accuracy of the information contained herein, Kenanga Futures Sdn Bhd does not warrant or represent expressly or impliedly as to the accuracy or completeness of the information. This information does not constitute financial or trading advice; neither does it make any recommendation regarding product(s) mentioned herein. Kenanga Futures Sdn Bhd does not accept any liability for any trading and financial decisions of the reader or third party on the basis of this information. All applicable laws, rules, and regulations, from local and foreign authorities, must be adhered to when accessing and trading on the respective markets.

Risk Disclosure:

Trading in contracts involves the risk of loss greater than your initial investment. This brief statement does not disclose all of the risks and other significant aspects of trading in contracts. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in contracts is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

For a full statement on risk disclosure, please refer to this link https://www.kenangafutures.com.my/wp-content/uploads/2020/09/RISK-DISCLOSURE-STATEMENT.pdf