KFSB Spotlight : Looking Ahead: 2023

Introduction

Central banks’ policy tightening and geopolitical events led to market sell-offs in 2022. In 2023, the outlook remains uncertain. From an energy crisis to surging inflation and an ongoing war, there is no shortage of opportunities and dangers in the market investors should be mindful of.

Russia-Ukraine War

The ongoing Russia-Ukraine conflict is showing no sign of any ending in sight, stoking fears that supply disruptions due to the war will continue to exert inflationary pressure on the global economy. Energy and agricultural commodities are likely to see more upside risks, should the conflict persist or intensify. While the war has largely been confined to Ukrainian territories, some have pointed to the possibility of a full-blown conflict on the European continent and a nuclear standoff.

1.0 Russia’s progress in Ukraine

BBC reported that Russia has suffered a major defeat in the south of Ukraine, withdrawing from the western Kherson region. According to New York Times, Ukraine has reclaimed 54 percent of the land Russia has captured since the beginning of the war. Losing Russia means higher chance that Putin might use nuclear weapons.

Source : (https://www.nytimes.com/interactive/2022/world/europe/ukraine-maps.html)

“Certainly, it would be a global disaster for humanity; a disaster for the entire world … as a citizen of Russia and the head of the Russian state I must ask myself: Why would we want a world without Russia?” -Putin, The World Order 2018

2.0 What Russia’s invasion of Ukraine means for agricultural and energy commodities

Russia’s invasion of Ukraine sent the price of commodities, including natural gas and wheat, through the roof. Russia supplies 40% of the natural gas to EU mostly by pipelines through Ukraine. According to the European Commission, Ukraine accounts for 10% of the world wheat market, 15% of the corn market, and 13% of the barley market.

Source : (https://www.icis.com/explore/resources/news/2019/09/23/10421334/icis-explains-eu-russia-and-ukraine-s-gas-transit-negotiations/)

China’s Recovery

For most of 2022, the “zero-COVID” strategy pursued by China, where cities were locked-down and businesses closed, severely strained the Chinese economy, supply chains and consumption, which have had global implications. By end of the year, the “zero-COVID” strategy had largely been dismantled, leading to a gradual reopening of the world’s second largest economy. An anticipated surge in COVID-19 infections, however, raises fears that dampened consumer confidence and economic activity will weigh on commodity prices and the wider economy.

1.0 When China fully reopens

Daniel Yergin, Vice Chairman of S&P Global says there’s a chance oil could go as high as $121 a barrel when China fully reopens, but warned there are three major uncertainties: The Federal Reserve’s decisions, China demand and Moscow’s reaction to the price caps. Oil demand from the world’s top importer could reach 15.7 million barrels per day in 2023, which is around 700,000 barrels higher than 2022, S&P said in its most recent forecast.

2.0 China may not be the driving factor

China, the largest commodities buyer that account for 11.37% of global imports, is undeniably a “price maker”. However, the reopening of Chinese economy might have limited impact on commodity prices as the main drivers behind the increases is supply-related.

Source : (https://marketnews.com/divergence-craters-between-chinese-imports-and-commodity-prices)

Inflation

As the world continues to grapple with high inflation levels, monetary policy will remain in focus in the year ahead. In a bid to cool surging prices, global central banks have been tightening financial conditions by substantially raising interest rates from near-zero levels that have been in place since the Great Recession. Now that inflation has seemingly moderated at the end of 2022, concerns that the dramatic rise in cost of borrowing may induce a recession have so far dashed hopes of a rebound in risky assets such as equities, which are struggling to recover from bear markets seen earlier in the year.

1.0 A supply-side problem

Manufacturers and suppliers were unable to produce and deliver goods efficiently during Covid lockdowns. In addition to that, sanctions on Russia, war in Ukraine, and underinvestment in oil and gas have reduced supply of commodities. Raising interest rates to curb inflation is not the right solution as high prices have been mainly driven by supply-side problem.

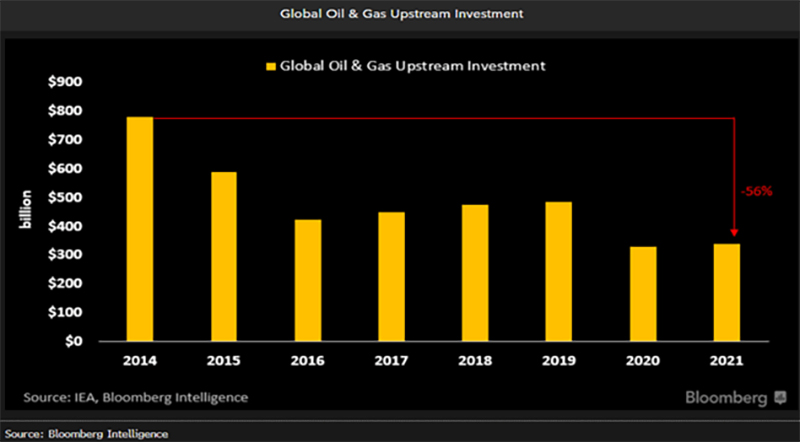

2.0 Underinvestment in oil and gas

According to JP Morgan head of oil and gas research Christyan Malek there is a $600 billion shortfall of upstream investment needed between 2021 and 2030 to meet global oil demand. According to IEA data, annual investment in upstream oil and gas has been in decline since 2014.

Source : (https://www.bloomberg.com/professional/blog/underinvestment-risks-global-energy-security-at-adipec/)

U.S. Dollar

The strength of the U.S. dollar, largely due to aggressive tightening by the Federal Reserve, is another important catalyst for market observers in more ways than one. For starters, many important commodities are dollar-denominated, of which the United States is among the largest consumers. Second, a strong dollar may hurt export-heavy U.S. companies as well as make U.S. financial assets less competitive than their foreign counterparts. Moreover, emerging markets are at greater risk of experiencing capital outflows, prompting action from their respective central banks and consequently destabilizing global financial markets.

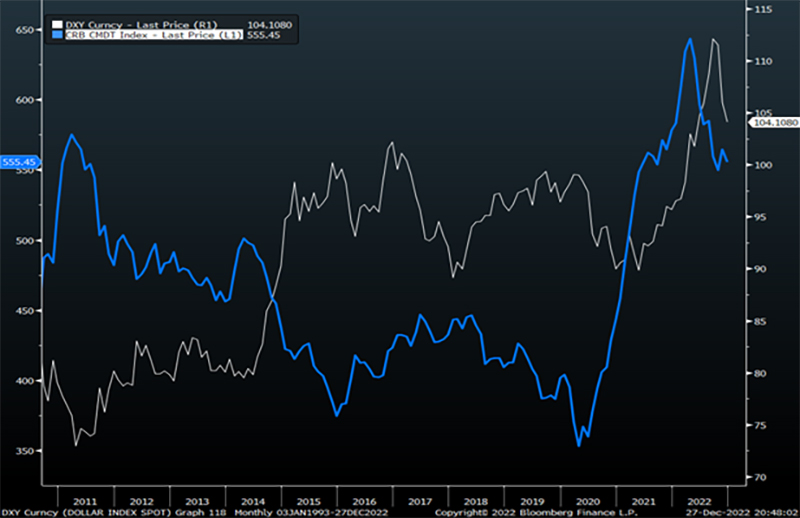

1.0 Correlation between dollar and commodities is gone

Most commodities are priced in dollar. Conventional wisdom tells us that a stronger dollar tends to keep price of dollar-denominated commodities lower, while a weaker dollar drives price of the commodities higher. In 2021, the inverse relationship between commodities and dollar broke down.

(Source: Bloomberg)

2.0 DXY components influence dollar

The U.S. Dollar Index (DXY) is a relative measure of the U.S. dollar strength against a basket of six influential currencies. DXY contains six component currencies: Euro, Japanese yen (JPY), British pound (GBP), Canadian dollar (CAD), Swedish krona (SEK) and Swiss franc (CHF). Euro is the largest component of the DXY, making up 57.6% of the basket, followed by JPY (13.6%) and GBP (11.9%). Euro is falling mainly because of EU reliance on Russian gas and the difference in interest rate levels in the US and the Eurozone, however the downtrend might reverse if Zelensky accepts the olive branch.

3.0 Strong dollar bad for emerging markets

A strong dollar is good for the US, but bad for the world. A strong dollar makes debt-ridden countries like Argentina, Egypt and Kenya at higher risk of default. Emerging markets relying on foreign investment and foreign capital suffer capital outflow due to strengthening dollar. According to BIS, increase of 1 percentage point in the value of the U.S. dollar can dampen the EM growth outlook by more than 0.3%. However, net importer of oil and commodities such as China and India might benefit from cheaper commodity prices.

Geopolitical Tensions

In a year that was dominated by the Russia-Ukraine war, other geopolitical events received comparatively less attention but are as important to financial markets. Among them is the Join Comprehensive Plan of Action (JCPOA), more commonly known as the Iran nuclear deal, which fell apart as a result of a withdrawal from the agreement initiated by the Trump Administration. Despite a long period of political wrangling and negotiations, the parties to the original agreement have yet been able to reach a new one, as sanctions against Iran remain in place, which has an impact on the supply side of the oil market. Furthermore, increased friction between OPEC and the West, particularly the United States, may lead to more volatility in energy markets.

1.0 U.S.-China relations

U.S.-China relations do not appear to have improved under the Biden Administration, especially after House Speaker Nancy Pelosi’s visit to Taiwan in August. With the recent chip export restriction and increasingly anti-China bipartisan Congress, relations have taken a turn for the worse. In the event China decides to retaliate, hundreds of billions of dollars worth of trade are at stake and we may see the return of a trade war, which would certainly have a tremendous impact on grain and other commodity markets.

Conclusion

Major events of 2023 would be an extension from the previous: namely the Russia-Ukraine war, China’s recovery, inflation, U.S. dollar strength, geopolitical tensions. Each of these catalysts presents desirable opportunities but also demands caution in the decision-making process.

This report has been exclusively created by Kenanga Futures Dealing Global Markets team.

Download full article here

Disclaimer:

This document has been prepared solely for the use of the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without the prior written permission from Kenanga Futures Sdn Bhd. Although care has been taken to ensure the accuracy of the information contained herein, Kenanga Futures Sdn Bhd does not warrant or represent expressly or impliedly as to the accuracy or completeness of the information. This information does not constitute financial or trading advice; neither does it make any recommendation regarding product(s) mentioned herein. Kenanga Futures Sdn Bhd does not accept any liability for any trading and financial decisions of the reader or third party on the basis of this information. All applicable laws, rules, and regulations, from local and foreign authorities, must be adhered to when accessing and trading on the respective markets.

Risk Disclosure:

Trading in contracts involves the risk of loss greater than your initial investment. This brief statement does not disclose all of the risks and other significant aspects of trading in contracts. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in contracts is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

For a full statement on risk disclosure, please refer to this link https://www.kenangafutures.com.my/wp-content/uploads/2020/09/RISK-DISCLOSURE-STATEMENT.pdf