Performance and Key Highlights of Bursa Malaysia Derivatives (BMD) Products in Q1 2022

Prepared By : Kenanga Futures Sdn Bhd

Global Highlights

Widening US Trade Deficit

US trade deficit reached a record USD$859.1 billion as of December 2022, an increase of 27.0% from the previous year. This was driven by pandemic-led robust domestic demand, rising energy prices & ongoing supply-chain disruptions.

Imports surged by $576.5 billion, or 20.5% from previous year, as both the quantity and the price of the foreign products that Americans purchased increased. Surge in U.S. goods trade deficit extends a surge in offshoring and has eliminated more than 5 million manufacturing jobs.

Indonesia Palm Oil Regulations (DMO)

Indonesia expanded Domestic Market Obligation (DMO) regulation by imposing higher export levy on all palm & palm kernel related exports in February 2022 to tackle the domestic shortage of cooking oil.

Exporters were required to sell an amount equal to 30% of their planned exports to the domestic market at a predetermined price of IDR 9,300 per kg for CPO and IDR 10,300 per kg for RBD Palm Olein.

Russia-Ukraine Geopolitical Tension

The ongoing Ukrainian crisis is threatening the availability of food and edible oil in countries that heavily rely on grain and other food exports from Ukraine and Russia. Ukraine and Russia jointly control 77% of world exports of sunflower oil, with Ukraine’s share being 48%.

Scarcity in sunflower oil and anxious Indian buyers, with no clarity on sunflower oil shipments out of Ukraine, turned to crude palm oil from Malaysia to fulfill demand. This has driven FCPO futures to reach record high of RM7,000/ton in February 2022

Malaysia Highlights

Emergency EPF withdrawals

Allowed special withdrawal by contributors from their Employees Provident Fund (EPF) amounting to RM10,000 in March 2022.

The Malaysian Government had previously allowed EPF withdrawal through three schemes, namely i-Lestari, i-Sinarand i-Citra amounting to RM101 billion, involving 7.34 million contributors since the Covid-19 pandemic that hit the country two years ago.

Foreign Labour Shortages

Sarawak, being the second largest palm oil producing state faced a shortage of 45,000 foreign workers. Despite CPO price surpass previous record of RM5,000/ton (Oct 2021), local producers missed the opportunity to enjoy the full benefit of the pricing as 20-30% of present palm fruits are left unharvested due to shortage of workers.

Malaysia & Indonesia signed an MoU in April 2022 to facilitate entry of workers in Q2 2022

Accommodative Overnight Policy Rate

Malaysia Central Bank maintained Overnight Policy Rate (OPR) at 1.75% as economic activity rebounded in Q4 2021 in line with the relaxation of previous containment measures.

Growth is expected to gain further momentum in 2022 driven by the expansion in global demand and higher private sector expenditure amid improvements in the labour market and continued policy support.

Source : Bloomberg, Reuters, BBC News The Edge Market and The Star

Overall Bursa Malaysia Derivatives Performance

QoQ Performance

No. of Contracts (#)

ADV

Quarterly End Open Interest

YoY Performance

No. of Contracts (#)

ADV

Quarterly End Open Interest

No. of Trading Days (#)

2022 (1st Qtr): 61 days

2021 (4th Qtr): 58 days

2021 (1st Qtr): 60 days

- Decline in the BMD market’s volume and open interest was partially due to the downward interest trend in the FCPO market, the leading listed derivatives product in Malaysia. This occurred due to the aftermath of the floods in December, slow momentum pick-up post the CNY festive period and uncertainty due the Russia –Ukraine geopolitical tensions.

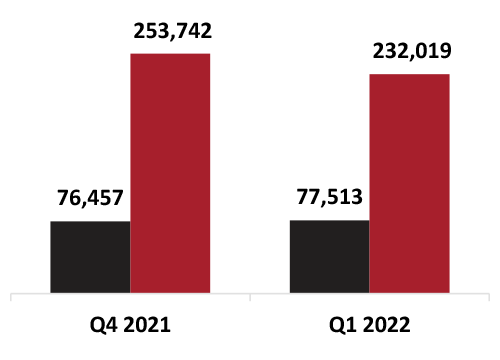

- Quarter-on-Quarter comparison:

- In terms of ADV, the number of contracts grew by 1.4% from 76,457 contracts in Q4 2021 to 77,531 contracts in Q1 2022

- Quarterly End Open Interest contracted by 8.6% from 253,742 contracts in Q4 2021 to 232,019 contracts in Q1 2022

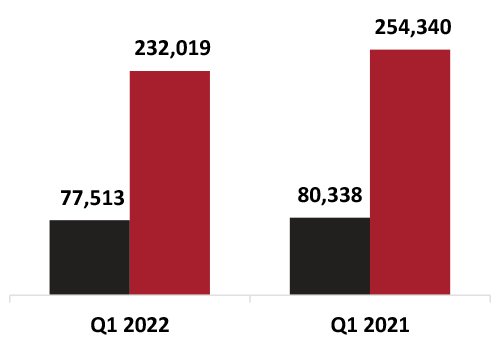

- Year-on-Year Comparison:

- ADV decreased by 3.5% from 80,338 contracts in Q1 2021 to 77,513 contracts in Q1 2022

- Quarterly End Open Interest contracted by 8.8% from 254,340 contracts in Q1 2021 to 254,340 contracts in Q1 2022

Source : Bursa Malaysia & The Edge Malaysia ((Ukraine-Russia conflict: A double-edged sword for commodities)

Overall BMD’s Market Demography

Participation rate (%)

Foreign Institutions

Domestic Institutions

Foreign Retail

Domestic Retail

Locals

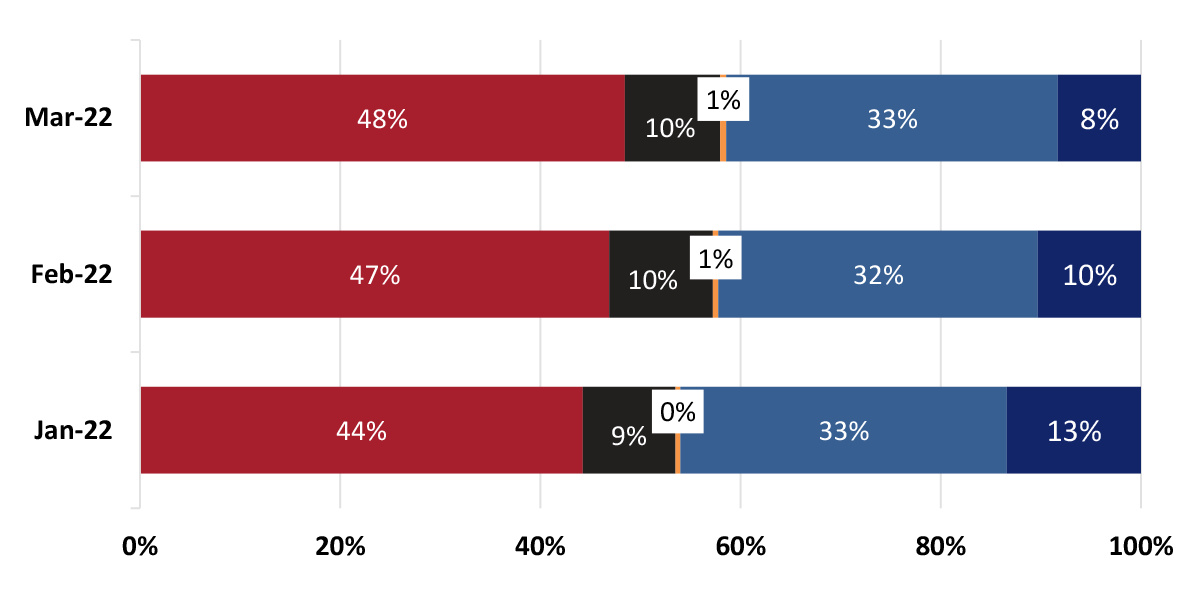

- BMD market continued to be dominated by foreign institution, where they consistently made up more than 45% on average of the market share of BMD in third quarter of the year

- Like Q4 2021, domestic retail remained to be the second largest participants of BMD market where they constituted around 30% in the three months of the year

- Behind domestic retail are domestic institution and local participants which claimed third (10%) and fourth (8%) largest of BMD market participants as at end March 2022

Source : Bursa Malaysia

Product Highlights Q1 2022

Crude Palm Oil Futures (FCPO)

FCPO, QoQPerformance

No. of Contracts (#)

ADV

Quarterly End Open Interest

FCPO, YoY Performance

No. of Contracts (#)

ADV

Quarterly End Open Interest

No. of Trading Days (#)

2022 (1st Qtr): 61 days

2021 (4th Qtr): 58 days

2021 (1st Qtr): 60 days

- CPO started the quarter on the higher end, supported by massive rallies in commodities as Russia’s invasion of Ukraine continues to roil global markets and fuel fears of supply crunches. The crisis had disrupted the supply of vegetable oil from the two countries, particularly sunflower oil, which has prompted demand for palm oil as a substitute.

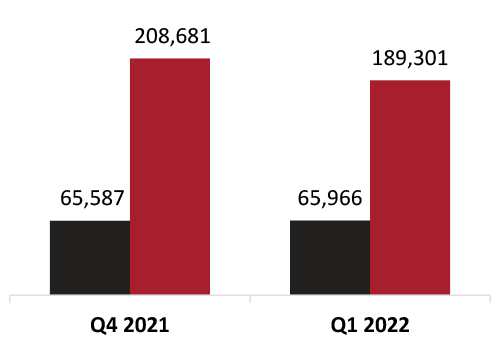

- Quarter-on-Quarter comparison:

- Number of contracts for ADV improve slightly by 0.6% from 65,587 in Q4 2021 to 65,966 in Q1 2022

- Quarterly End Open Interest declined by 9.3% compared to the previous quarter. Number of contracts declined from 208,681 in Q4 2021 to 189,301 in Q1 2022

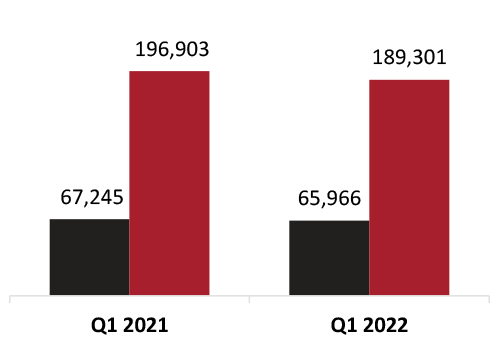

- Year-on Year comparison:

- ADV for first quarter this year registered 65,587 contracts traded, a decline of 2.5% compared to the same quarter in 2020

- Quarterly End Open Interest declined by 3.9% from 196,903 contracts in Q1 2021 to 189,301 contracts in Q1 2022

Source : Bursa Malaysia, The Edge Malaysia & Economic Times (Sunflower oil: Supply disruption by Russia-Ukraine conflict could shorten supply of Sunflower oil

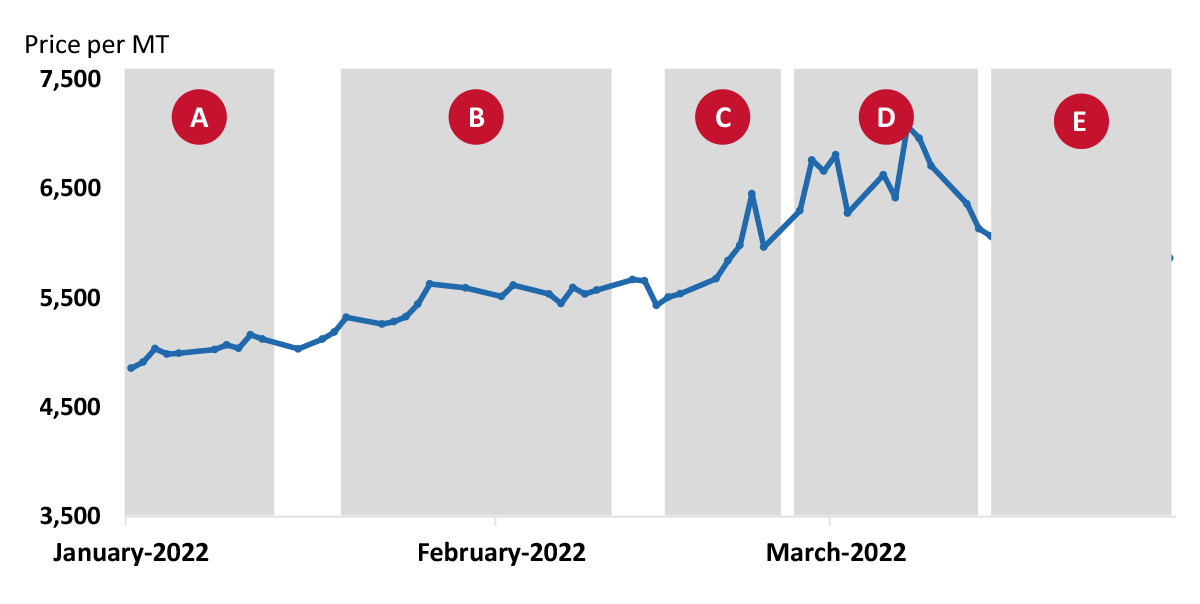

FCPO Q1 2022 Performance

Snapshot of FCPO Performance

Price as at 31/03/2022 (Last trading day): 5,705

Quarter High (9 Mar 2022): 7,268

Quarter Low (3 Jan 2022): 4,857

Q1 2022 Performance (% change): +45.6%

|

A |

3-Jan-2022 to 21-Jan-2022 (+9.57%) FCPO market began Q1 2022 in a moderately high note driven by shortages in supply (caused by the flooding & labourshortages etc.) in second-biggest grower Malaysia |

|

B |

24-Jan-2022 to 16-Feb-2022 (+3.29%) Broke through the RM5,000 level driven by stronger soybean oil and petroleum prices, reduced supplies from top producer Indonesia & India’s surging demand for tropical oil following import tax cuts |

|

C |

18 Feb 2022 to 28 Feb 2022 (+13.71%) Continued growth despite weaker production outlook for South American corn and soybean. Indonesia expanding export permit requirement for all palm oil products |

|

D |

01 Mar 2022 to 16 Mar 2022 (+10.27%) Rose to the costliest among the 4 major edible oils as buyers rush to secure replacements for sunflower oil shipments due to Russia’s invasion of Ukraine |

|

E |

17 Mar 2022 to 31 Mar 2022 (-20.86%) Retreated on concerns about demand destruction from record high prices (e.g., expectations of shrinking stockpiles from 2ndbiggest grower Malaysia & escalating tensions in the Black Sea region) |

Source : Bloomberg, The Edge Market (https://www.theedgemarkets.com/flash-categories/vegoils)

FCPO, Market Demography Q1 2022

Participation rate (%)

Foreign Institutions

Domestic Institutions

Foreign Retail

Domestic Retail

Locals

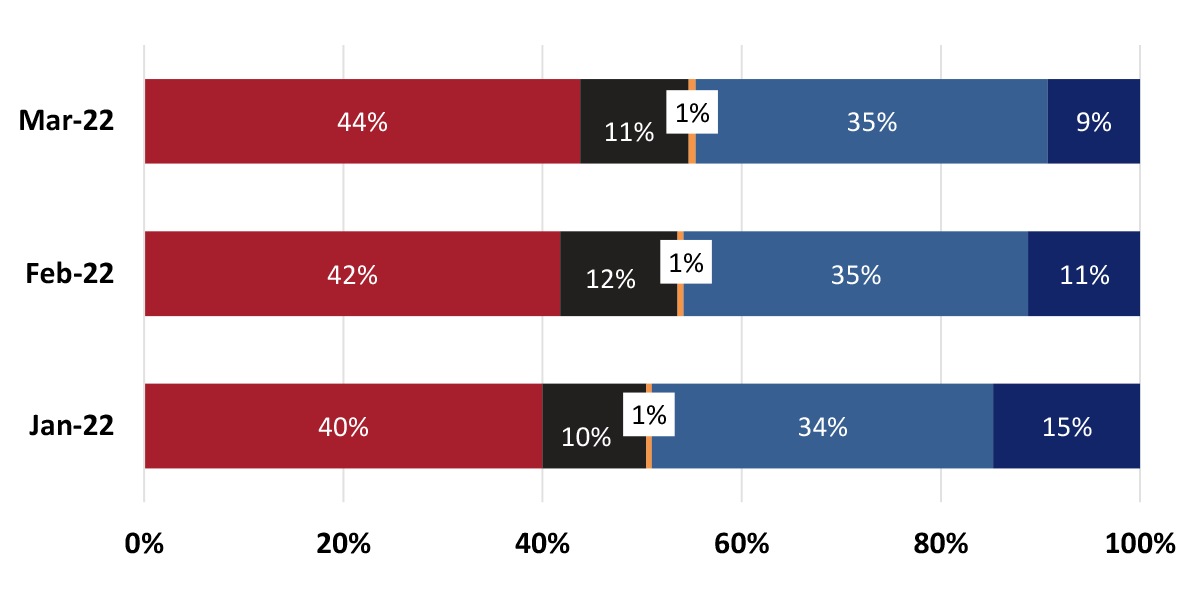

- Similar narrative from BMD market was recorded in the Crude Palm Oil Futures market (FCPO) when foreign institution and domestic retails maintained their position as the largest and the second largest of FCPO market’s participants in Q1 2022 respectively.

- Foreign institution continue to dominate the participation rate and makes up at least 40% of the market share in Q1 2022,while domestic retail segments were able to consistently maintain over 30% of the market share

- Similar to the overall derivatives market, domestic institutions are the third largest participants in the FCPO market as they consistently made up around 11% of market share every month in the first quarter of the year

- As of March 2022, locals were the fourth largest participants of FCPO market making up 9% of the total participation rate, followed by foreign retail participations of 1%

Source : Bursa Malaysia

Product Highlights Q1 2022

FTSE Bursa Malaysia KLCI Futures (FKLI)

FKLI, QoQ Performance

No. of Contracts (#)

ADV

Quarterly End Open Interest

FKLI, YoY Performance

No. of Contracts (#)

ADV

Quarterly End Open Interest

No. of Trading Days (#)

2022 (1st Qtr): 61 days

2021 (4th Qtr): 58 days

2021 (1st Qtr): 60 days

- Trading in first quarter was mainly subdued, taking cue from external market amid heightened market volatility in the region while tracking the movements on Wall Street. Optimism about economic recovery after the announcement on the reopening of Malaysia’s borders on April 1, 2022 along with government’s plan on entering the ‘Transition to Endemic’ phase and rising crude oil prices provided a much needed boost to the market.

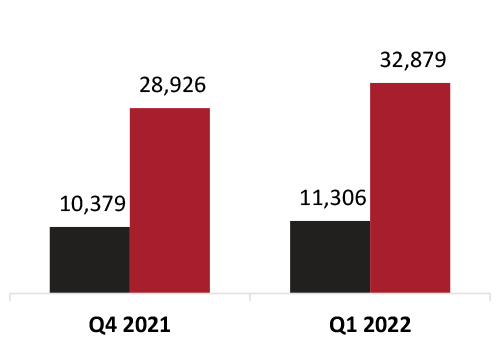

- Quarter-on-Quarter comparison:

- ADV increased by 8.9% in first quarter this year to 11,306 contracts, compared to 10,379 contracts in fourth quarter 2021

- In terms of Quarterly End Open Interest, the number of contracts increased by 13.7% from 28,926 contracts in Q4 2021 to 32,879 contracts in Q1 2022

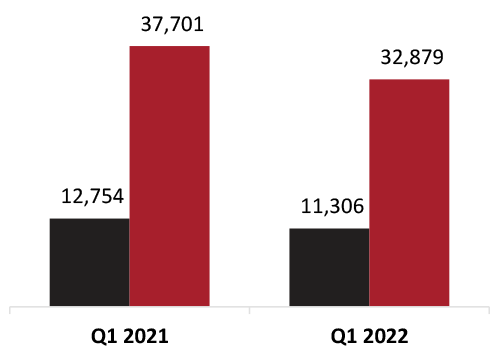

- Year-on Year comparison:

- On Y-o-Y perspective, the ADV registered a 11.4% dropped in its number of contracts to 11,306 contracts in Q1 2022 from 12,754 contracts in the same quarter in 2021

- Similarly, Quarterly End Open Interest also declined by 12.8% from 37,701 contracts in Q1 2021 to 32,879 contracts in Q1 2022

Source : Bursa Malaysia , The Edge Malaysia , The Star (Bursa, global equities dive on reports of ‘full-scale invasion’ of Ukraine)

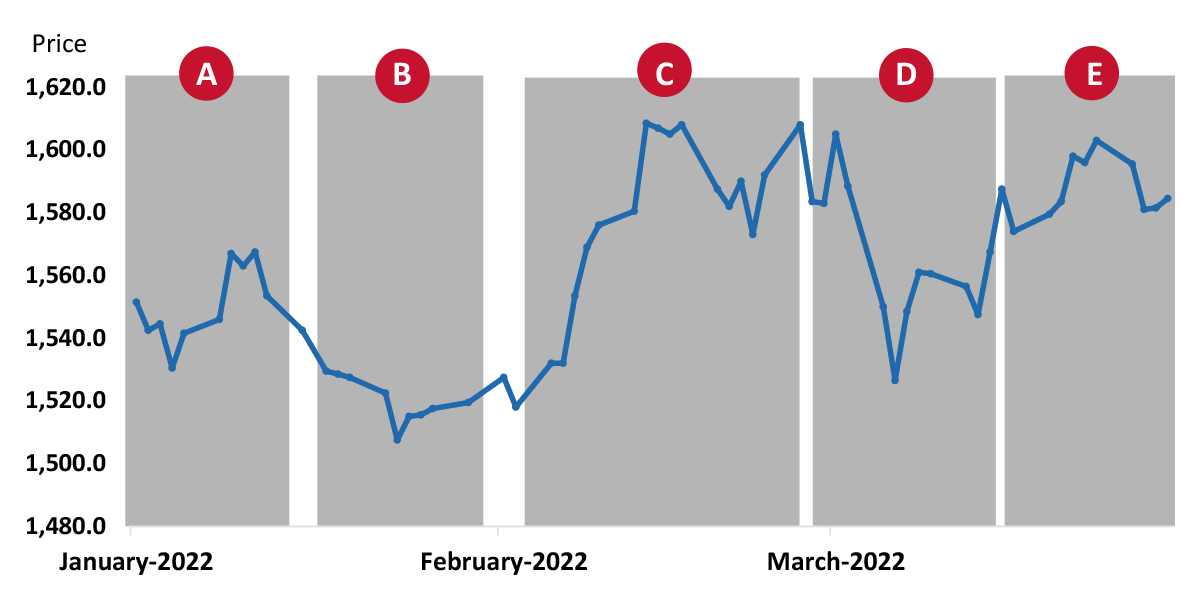

FKLI Q1 2022 Performance

Snapshot of FCPO Performance

Price as at 31/03/2022 (Last trading day): 1,581

Quarter High (9 Mar 2022): 1,620

Quarter Low (3 Jan 2022): 1,500

Q1 2022 Performance (% change): +2.9%

|

A |

03 Jan 2022 to 13 Jan 2022 (+1.03%) FKLI in negative territory as regional sentiment dampened by US bond tapering, but continuous buying support in selected heavyweights led the index higher |

|

B |

15 Jan 2022 to 31 Jan 2022 (-1.50%) Market in a downtrend due to weak investor sentiment amid inflationary pressure & geopolitical concerns ahead of the US Fed Open Market Committee (FOMC) meeting |

|

C |

03 Feb 2022 to 28 Feb 2022 (+5.27%) Beginning of February saw a positive momentum allowing the FKLI to reach 1,608 lifted by heavy weights performance and global investors bargain hunt for financial sector stocks. Market corrected in the 2nd half of February due to the emergence of new variant Omicron & with new cases recorded over 28,000. |

|

D |

02 Mar 2022 to 17 Mar 2022 (-2.84%) FKLI traded in choppy session on continued selling pressure with all global indices in negative territory, arising from Russia-Ukraine’s conflict & rising inflationary pressures |

|

E |

18 Mar 2022 to 31 Mar 2022 (+1.04%) Market re-bounded to trade higher in the final period of Q1 driven by bargain-hunting & improved market sentiments in anticipation of borders re-opening |

Source : Bloomberg, The Edge Market (https://www.theedgemarkets.com/flash-categories/market-close)

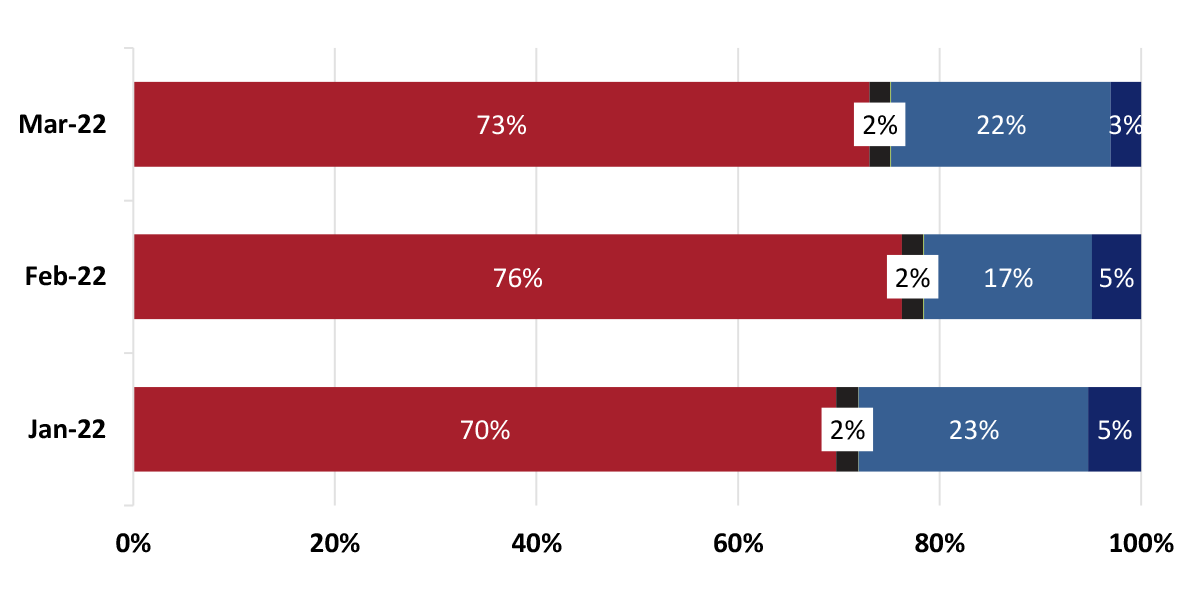

FKLI, Market Demography Q1 2022

Participation rate (%)

Foreign Institutions

Domestic Institutions

Foreign Retail

Domestic Retail

Locals

- Composition of the FKLI market demographic in Q4 2021 is similar to that in the previous quarters, where foreign institution continued to capture 70% of the market share

- Similar to overall BMD market, domestic retails remained to be the second largest FKLI market’s participant with more than 20% of participation rate in first quarter of 2022

- Meanwhile, both locals and domestic institutions maintained their third and fourth largest participants, accounting for 3% and 2% respectively as at end March 2022

Source : Bursa Malaysia

Industry Highlights & Developments

BMD Palm Oil Conference 2022 (POC)

BMD organised & hosted the Palm and Lauric Oils Price Outlook Conference & Exhibition (POC) in Kuala Lumpur from the 7th -9th March

Attended by policy makers, practitioners & thought leaders in the global edible oils industry to address industry’s challenges & opportunities

9 of the keynote speakers predicted CPO price in 2022 will trade between RM 4,000/ton to RM 9,427/ton which averages to RM 5,836/ton — 32% increase from average CPO prices in 2021 with majority being bullish on the price outlook

FCPO Recorded A New All Time High Price

Palm oil futures registered highest record in history during Q1 2022 with the third-month benchmark contract (FCPOc3) front month hitting RM 7268/ton

Recent bull run driven by Russia—Ukraine’s conflict, fears of global vegetable oil shortages, tightening of supply due to Indonesia’s export restrictions, weather concerns in South America & strong gains in external rival oils and the crude oil market

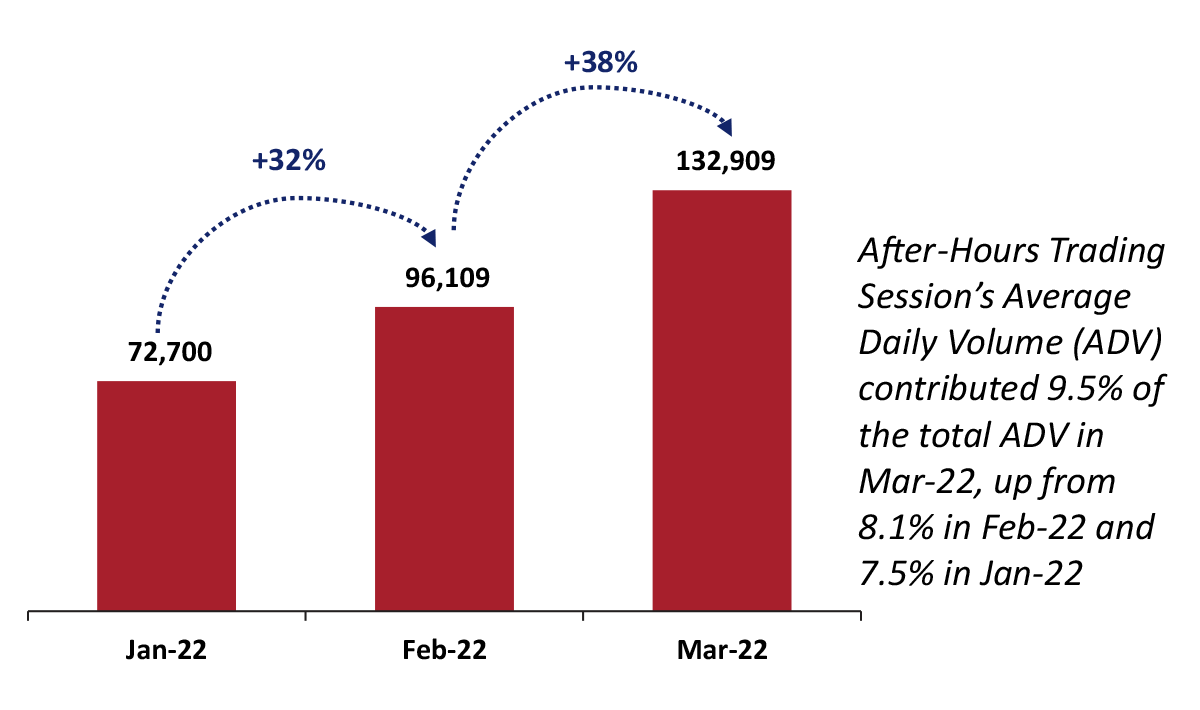

After Hours (T+1) Trading Session Success

BMD launched the highly anticipated T+1 session to enhance the competitiveness & attractiveness of the Exchange’s products among local and international traders on 6th Dec 2021

Market participants are able to trade BMD products between 9.00pm to 11.30pm from Monday to Thursday

T+1 Trading Session has witnessed a total of 301,718 contracts traded from Jan to Mar 2022, witnessing an of 35% m-o-m growth

After-Hours (T+1) Night Trading Session Volume

Contracts Traded (#)

Source : Bursa Malaysia

Download full article here

Disclaimer:

This document has been prepared solely for the use of the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without the prior written permission from Kenanga Futures Sdn Bhd. Although care has been taken to ensure the accuracy of the information contained herein, Kenanga Futures Sdn Bhd does not warrant or represent expressly or impliedly as to the accuracy or completeness of the information. This information does not constitute financial or trading advice; neither does it make any recommendation regarding product(s) mentioned herein. Kenanga Futures Sdn Bhd does not accept any liability for any trading and financial decisions of the reader or third party on the basis of this information. All applicable laws, rules, and regulations, from local and foreign authorities, must be adhered to when accessing and trading on the respective markets.

Risk Disclosure:

Trading in contracts involves the risk of loss greater than your initial investment. This brief statement does not disclose all of the risks and other significant aspects of trading in contracts. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in contracts is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

For a full statement on risk disclosure, please refer to this link https://www.kenangafutures.com.my/wp-content/uploads/2020/09/RISK-DISCLOSURE-STATEMENT.pdf