Performance and Key Highlights of Bursa Malaysia Derivatives (BMD) Products in Q4 2021

Prepared By : Kenanga Futures Sdn Bhd

Q4 2021 Market Review

Global Highlights

1) Emergence of New COVID-19 Variant Omicron

- On 24 November 2021, a new variant of SARS-CoV-2 was reported to World Health Organisation (WHO) where the variant was first discovered in Bostwana and South Africa.

- The variant, which was later being named as Omicron, was classified as Variant of Concern (VOC) and according to the US Centers for Disease Control and Prevention (CDC), Omicron likely spreads more easily that the original COVID-19 virus.

- So far, health experts still do not have a clear idea on how effective the vaccines are against Omicron.

2) Federal Reserve Began to be More Hawkish in their Stance

- Despite of uncertainty continued to shroud the market, US Federal Reserve (Fed) decided to adopt a more hawkish stance towards monetary policy.

- Most of the year 2021 saw Fed often adopted Dovish in light of the slowing economy. However, the Fed had accelerated their effort to taper by USD 30 billion per month where the process could be concluded by March 2022.

- The process gave clear indication that federal fund rate could be increased anytime in 2022.

3) Turkish Lira Crisis

- Turkey’s beleaguered currency has been plunging to all-time lows against the US dollar and the euro in recent months as it has lost 40% of its value since the start of the year, becoming one of the world’s worst-performing currencies.

- Turkey’s Central Bank has cut borrowing costs by 4% points since September, in line with Erdogan’s wishes, even though inflation accelerated to around 20%.

- The Turkish economic crisis and slumping lira will impact on bilateral trade, as the cost of imported goods will rise significantly in Turkish lira terms due to the sharp currency depreciation this year.

Malaysia Highlights

1) Massive Floods Hit Malaysia

- An extremely heavy rain occurred in Malaysia on 17 and 18 December 2021 which caused massive floods in eight states in the country with Selangor was the hardest state hit by the flooding.

- It was reported more than 50,000 people have been forced from their homes, while the number of deaths was reported to be more than 50 people.

- According to many analysts, the floods might caused several corporates to take a beat in the fourth quarter with manufacturing, plantations and tourism are among the industries that would experience largest impact from flooding.

- The estimated loss to Malaysia was between RM5.3 billion and RM6.5 billion.

Overall BMD Performance Q4 2021

No of Trading Days

Q4 2021 : 58

Q3 2021 : 62

Q4 2020 : 64

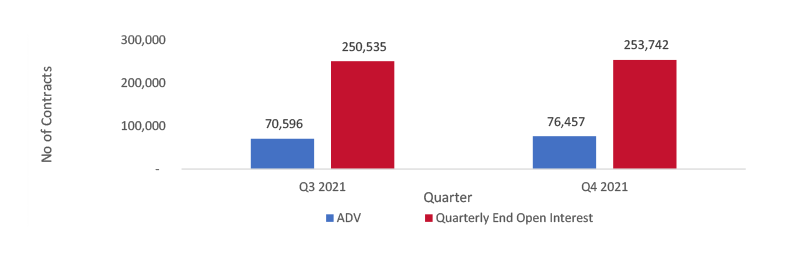

QoQ Performance

- BMD showed a good performance in its ADV and quarterly end open interest growth when Q-o-Q comparison is made.

- In terms of its ADV, the number of contracts grew by 8.30% from 70,596 contracts in Q3 2021 to 76,457 contracts in Q4 2021.

- Meanwhile, the quarterly end open interest also grew by 1.28% from 250,535 contracts in Q3 2021 to 253,743 contracts in Q4 2021.

YoY Performance

- The same performance was shown in Y-o-Y basis as both BMD’s ADV and quarter end open interest improved respectively.

- The ADV increased by 7.72% from 70,980 contracts in Q4 2020 to 76,457 contracts in Q4 2021.

- Meanwhile, the quarterly end open interest also grew by 22.68% from 206,837 contracts in Q4 2020 to 253,742 contracts in Q4 2021.

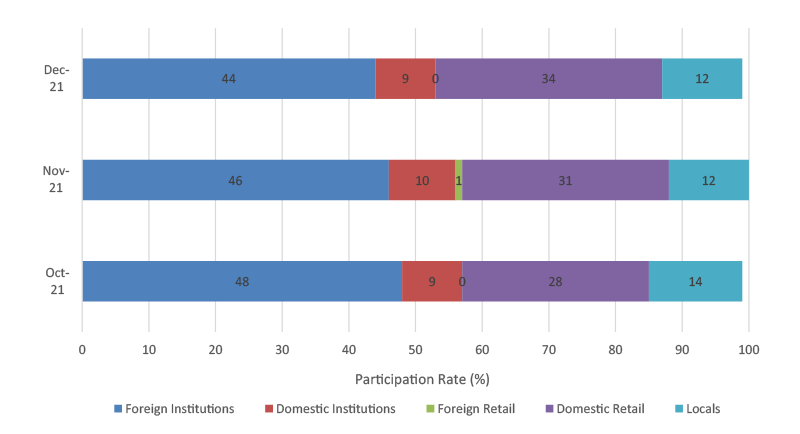

Overall BMD Market Demography Q4 2021

Review:

- BMD market continued to be dominated by foreign institution, where they consistently made up more than 45% on average of the market share of BMD in third quarter of the year.

- Like Q3 2021, domestic retail remained to be the second largest participants of BMD market where they constituted around 30% in the three months of the year.

- Behind domestic retail are domestic institution and local participants which claimed third and fourth largest of BMD market participants.

FCPO Performance Q4 2021

No of Trading Days

Q4 2021 : 58

Q3 2021 : 62

Q4 2020 : 64

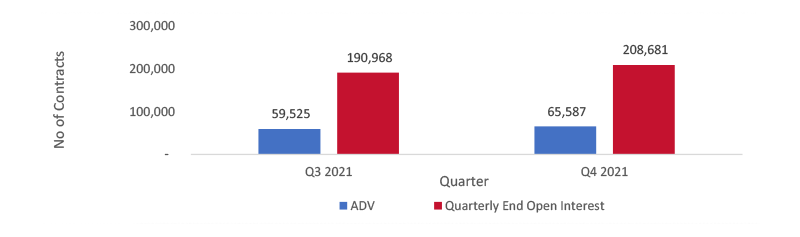

QoQ Performance

- FCPO shown a stellar performance in both ADV and quarterly end open interest growth on Q-o-Q basis.

- The number of contracts for ADV and quarterly end open interest improved by 10.18% and 9.28% respectively.

- The ADV for FCPO registered 65,587 contracts in Q4 2021, compared to 59,525 contracts in Q3 2021, while the quarterly end open interest recorded 208,681 contracts in Q4 2021, compared to 190,968 contracts in Q3 2021.

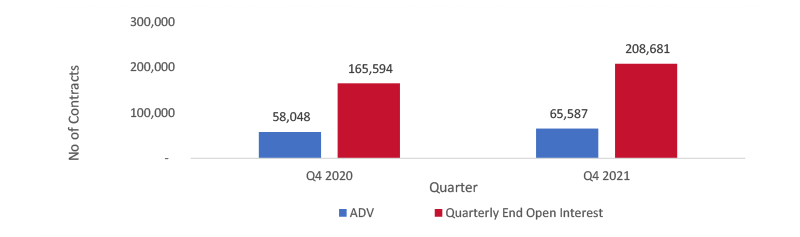

YoY Performance

- Similarly, FCPO showed outstanding growth in its both ADV and quarterly end open interest in Y-o-Y basis.

- The ADV for fourth quarter this year registered 65,587 contracts traded, a growth of 12.99% from the same quarter in 2020.

- Meanwhile, the quarterly end open interest improved by 26.02% from 165,594 contracts in Q4 2020 to 208,681 contracts in Q4 2021.

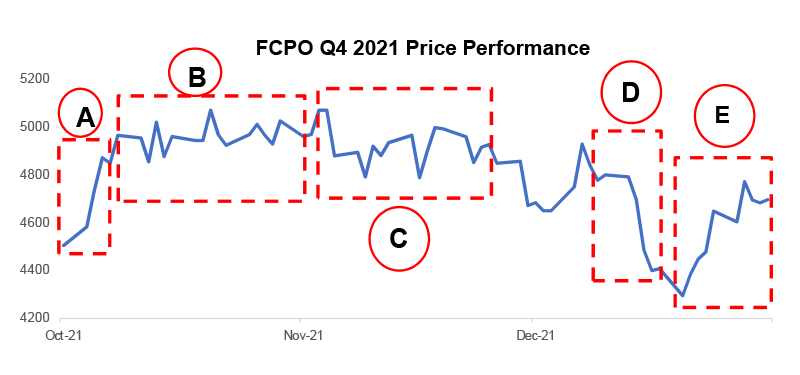

FCPO Q4 2021 Price Performance

Snapshot of FCPO Performance

Price as at 30/12/2021 (Last trading day): 4,697

Quarter High: 5,071 (03/11/2021)

Quarter Low: 4,295 (20/12/2021)

Q4 2021 Performance (% Change): +4.26

|

Period |

Remarks |

|---|---|

| A |

1 Oct 2021 to 8 Oct 2021 (+10.23%) FCPO market began the last quarter of the year in a stronger note as export data showed a positive record due to the increase intake from India ahead of their festive season and the shifting of palm oil imports from Indonesia to Malaysia. |

|

B |

12 Oct 2021 to 4 Nov 2021 (+4.45%) FCPO continue to rise to break the RM5,000 level mark after the Indian government decided to cut import duties for edible oils effective from 14 Oct 2021 from 24.75% to 8.25%. |

|

C |

8 Nov 2021 to 26 Nov 2021 (-0.94%) FCPO traded in a choppy session tracking the weakness in rival soybean oil market and higher production figures from MPOB, but the downside of the market was limited by the strong export data for the first half of the month. |

|

D |

10 Dec 2021 to 20 Dec 2021 (-10.52%) FCPO plunged to its lowest level in fourth quarter of the year affected by the weakness in rival vegetable oil market amid the surging in Omicron cases, while the weaker-than-expected export palm oil data had also dragged the market |

|

E |

21 Dec 2021 to 31 Dec 2021 (7.14%) FCPO retreated from the previous session’s losses in expectations of a softer December output due to harvest disruptions after the weekend’s floods affecting eight states in Malaysia. |

FCPO Market Demography Q4 2021

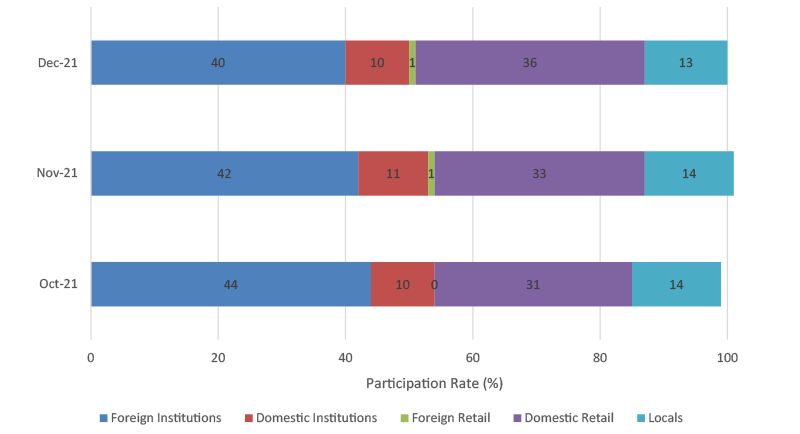

Review:

- The same narrative from BMD market was recorded in the FCPO market when foreign institution and domestic retails maintained their position as the largest and the second largest of FCPO market’s participants in Q4 2021.

- The domination of foreign institution can be seen when they managed to continue to make up atleast 40% or more of the market share in Q4 2021,while domestic retails were able to consistently constitute above 30% of the market share.

- However, unlike the overall BMD market, local participants are the third largest participants in FCPO market as they consistently made up around 13% of market share every month in the third quarter of the year.

- Meanwhile, domestic institutions were the fourth largest participants of FCPO market in Q3 2021.

FKLI Performance Q4 2021

No of Trading Days

Q4 2021 : 58

Q3 2021 : 62

Q4 2020 : 64

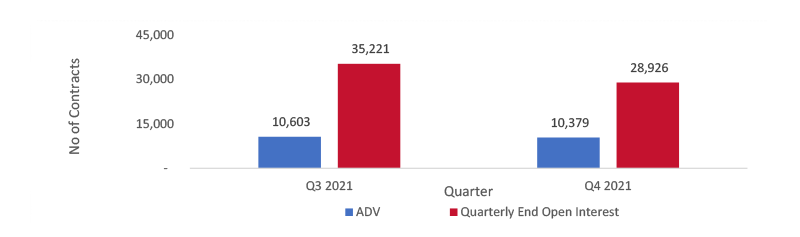

QoQ Performance

- Unlike FCPO, FKLI recorded negative growth in its ADV and quarterly end open interest in terms of Q-o-Q basis.

- The ADV dropped by 2.11% in fourth quarter this year to 10,379 contracts, compared to 10,603 contracts in third quarter this year.

- In terms of quarterly end open interest, the number of contracts dropped by 17.87% from 35,221 contracts in Q3 2021 to 28,926 contracts in Q4 2021.

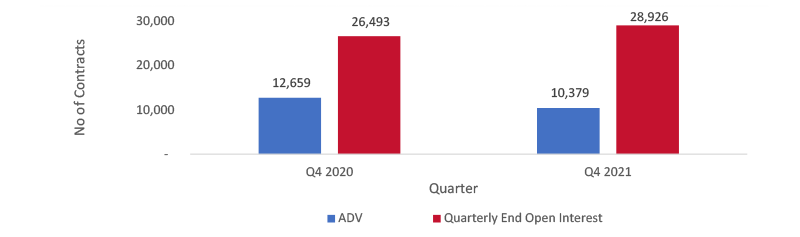

YoY Performance

- On Y-o-Y perspective, the ADV registered 18.01% dropped in its number of contracts to 10,379 contracts in Q4 2021 from 12,659 contracts in Q4 2020.

- However, the quarterly end open interest improved by 9.18% from 25,493 contracts in Q4 2020 to 28,926 contracts in Q4 2021.

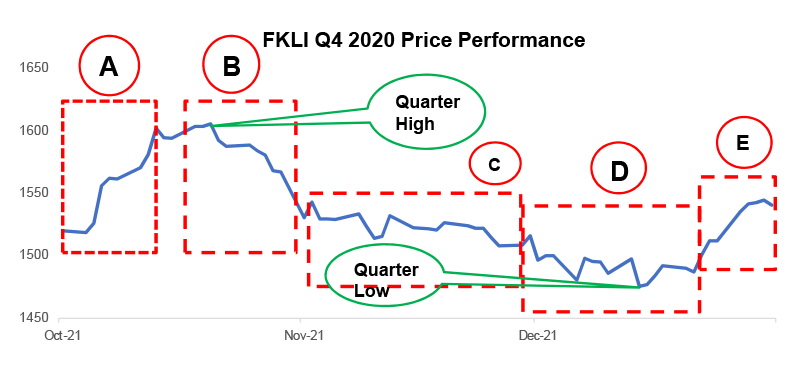

FKLI Q4 2021 Price Performance

Snapshot of FKLI Performance

Price as at 30/12/2021 (Last trading day): 1,540.50

Quarter High: 1,605.50 (20/10/2021)

Quarter Low: 1,475.50 (14/12/2021)

Q4 2021 Performance (% Change): +1.35

|

Period |

Remarks |

|---|---|

| A |

4 Oct 2021 to 13 Oct 2021 (+5.50%) The rising of FKLI market was driven by the surging of oil prices and the growing domestic economic optimism following the announcement of travelling curb relaxation. |

|

B |

20 Oct 2021 to 1 Nov 2021 (-4.67%) Market was in a downtrend due to profit taking activities, while investors remain cautious ahead the announcement of Budget 2022 by the government. |

|

C |

2 Nov 2021 to 26 Nov 2021 (-2.27%) Market reacted negatively after the announcement of one-off prosperity tax in Budget 2022, while lack of fresh trading catalyst had also caused market to remain stagnant. |

|

D |

30 Nov 2021 to 20 Dec 2021 (-1.72%) FKLI was traded in a choppy session due to concerns over possible halt on global economic recovery due to emergence of new Covid-19 variant Omicron. |

|

E |

21 Dec 2021 to 31 Dec 2021 (+3.60%) Market bounced back to trade higher in the final week of the year driven by bargain-hunting and window-dressing activities due to cheap valuations of the local market as compared to regional peers. |

FKLI Market Demography Q4 2021

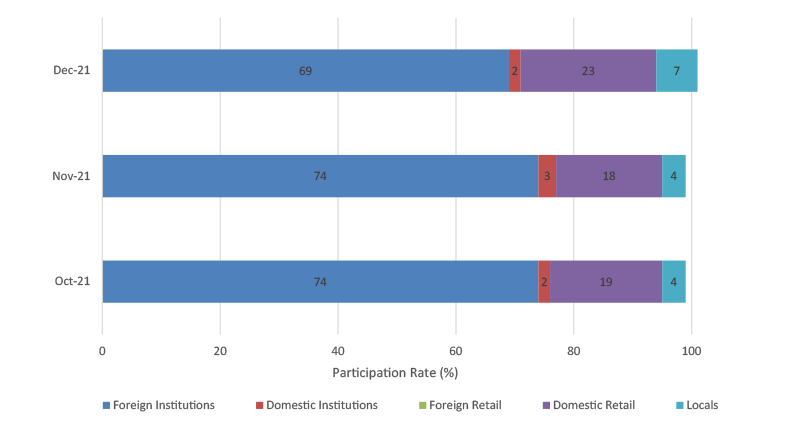

Review:

- The composition of the FKLI market demographic in Q4 2021 is similar to that in the previous quarters, where foreign institution continued to capture 70% of the market share.

- Similar to overall BMD market, domestic retails remained to be the second largest FKLI market’s participant with more than 20% of participation rate in Q4 2021.

- Meanwhile, both locals and domestic institutions maintained their third and fourth largest participants, respectively.

1

The Launch of East Malaysia Crude Palm Oil Futures (FEPO)

- To meet the needs of the East Malaysian palm oil market players for risk management tool, Bursa Malaysia Derivatives Berhad (BMD) had launched FEPO contract on 4th October 2021.

- According to BMD, the contract specification is similar to the existing Crude Palm Oil futures (FCPO) contract, except that FEPO will cater the physical deliveries in Sabah and Sarawak through three designated ports namely Bintulu, Lahad Datu and Sandakan.

2

The Launch of After-Hours (T+1) Night Trading Session

- On 6th December 2021, BMD had successfully launched its highly anticipated T+1 session to enhance the competitiveness and attractiveness of the Exchange’s products among local and international traders.

- The After-Hours trading offered by BMD is an extension of the Exchange’s current market trading hours in line with global market practices.

- Market participants are now be able to trade BMD products between 9.00 pm to 11.30 pm from Monday to Thursday.

- The After-Hours (T+1) Trading Session that was introduced, has since seen a total of 51,006 contracts traded in December 2021, contributing 5% of the day and night average daily trading volume in the same period.

Download full article here

Disclaimer:

This document has been prepared solely for the use of the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without the prior written permission from Kenanga Futures Sdn Bhd. Although care has been taken to ensure the accuracy of the information contained herein, Kenanga Futures Sdn Bhd does not warrant or represent expressly or impliedly as to the accuracy or completeness of the information. This information does not constitute financial or trading advice; neither does it make any recommendation regarding product(s) mentioned herein. Kenanga Futures Sdn Bhd does not accept any liability for any trading and financial decisions of the reader or third party on the basis of this information. All applicable laws, rules, and regulations, from local and foreign authorities, must be adhered to when accessing and trading on the respective markets.

Risk Disclosure:

Trading in contracts involves the risk of loss greater than your initial investment. This brief statement does not disclose all of the risks and other significant aspects of trading in contracts. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in contracts is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

For a full statement on risk disclosure, please refer to this link https://www.kenangafutures.com.my/wp-content/uploads/2020/09/RISK-DISCLOSURE-STATEMENT.pdf