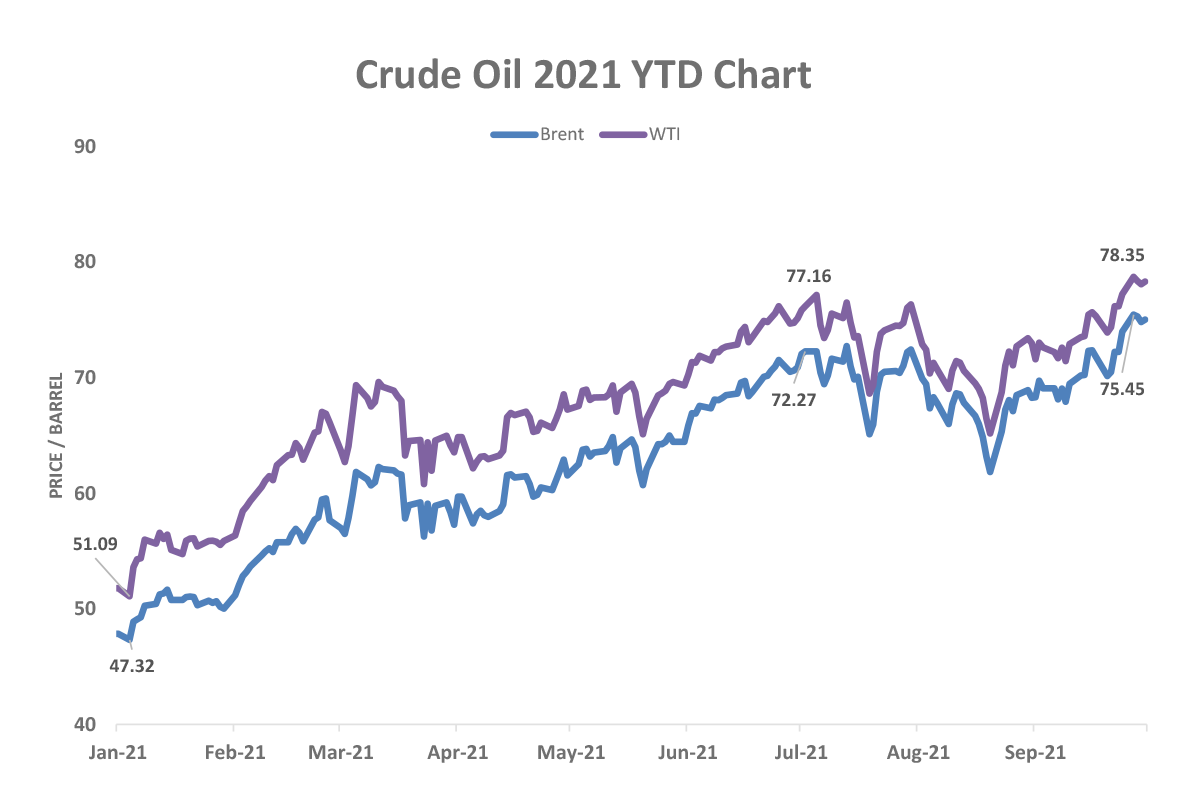

KF Spotlight : WTI & Brent Crude Oil – YTD 2021 Market Recap

Oil prices have rallied sharply higher this year with Brent oil up 51% year-to-date (YTD) and WTI Crude advancing 55% YTD, largely due to tight oil supply by OPEC, especially from Saudi Arabia and Russia, and improving oil demand as economic growth marches towards new normality.

After several months of steadily increasing prices, volatility heightened in July when members of OPEC+ initially concluded their ministerial meeting in July without reaching an agreement on future production cuts and adjustments to baseline production levels. However, the members later announced they had reached an agreement to ease production cuts by 400,000 barrels per day (b/d) each month, beginning in August 2021. The agreement also included adjustments to the baseline crude production levels of some OPEC+ members, including Saudi Arabia, Russia, and the United Arab Emirates, to take effect in May 2022.

Meanwhile, rising cases of the Delta variant of the COVID-19 virus presented an additional downside price risk because of potentially lower demand for petroleum, which add to the volatility. As such, the risk of lower demand contributed to the decline in prices in late July and early August.

Source : Bloomberg

FACTORS THAT AFFECTED THE MARKET

The Wrangle in in OPEC

In 2020, OPEC + countries agreed to reduce output by 10 mb/d from May 2020 to end of April 2022, to contain the price decline caused by falling demand. Now, with global demand reviving, Saudi Arabia has proposed that OPEC increase production by 2 mb/d between August 2021 to December 2021, but extend rest of the cuts until the end of 2022. But the UAE wants the production cuts to extend until end of 2022 only if the baseline for output is revised. OPEC members’ productions are linked to the baseline and this was to be revised at the end of the current production cut agreement, which was April 2022. Extending the cuts until end of next year would result in the UAE not being able to pump more oil, thus leading to under-utilisation of its production capacity.

While the supply situation is not unsalvageable, demand projections may need downward revision if the third wave or new variants of the virus cause further disruptions in global recovery. Also, the recovery is limited to advanced economies with most developing and under-developed nations yet to progress materially in vaccination. Global travel cannot revive under these conditions.

Source : U.S Energy Information Administration (EIA)

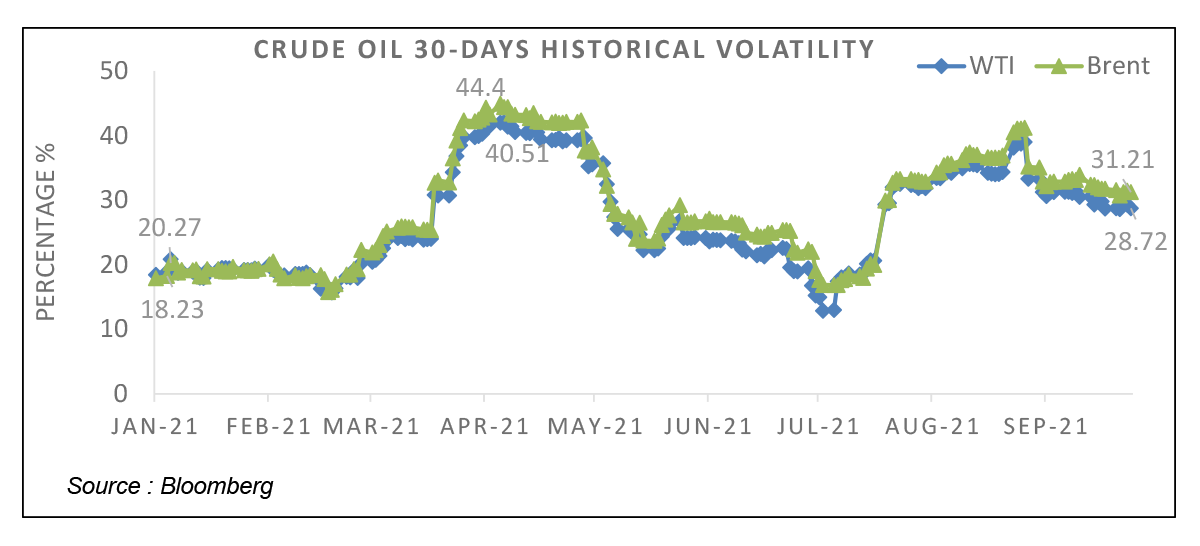

Crude Oil Historical Volatility

July’s OPEC+ announcements and heightened uncertainty in the COVID-19 outlook with rising cases of new viral variants have likely contributed to heightened uncertainty and price volatility. The 30-day historical volatility for WTI crude oil futures prices rose above 30% on July 19, and volatility for Brent crude oil followed suit. Both benchmarks had historical volatility less than 30% throughout June and most of May. As of August, WTI 30-day historical volatility was 38%, and Brent 30-day historical volatility was 36%, up 18 percentage points and 23 percentage points, respectively, compared with the beginning of July.

Source : U.S Energy Information Administration (EIA)

Demand – Supply Equation

Global demand for oil declined from 99.7 million barrels per day (mb/d) in 2019 to 91 mb/d in 2020 as the Covid-19 pandemic dealt a sharp blow. Travel and mobility were among the worst affected by the lockdowns, constricting petroleum consumption. With crude oil prices crashing, supplies were reduced in the second quarter of 2021, by both OPEC and non-OPEC producers.

The sharp rally in petroleum price in 2021 is due to two primary factors. One, the virus seems to have been contained quite effectively since the beginning of this year, especially in the OECD countries which account for around 47% of demand. The fast pace of vaccination has helped revive economic activity in these countries, leading to expectation of good demand for petroleum products. The IEA, in its June report, expects global oil demand to return to pre-pandemic levels by the end of 2022, rising 5.4 mb/d in 2021 and a further 3.1 mb/d in 2022.

Two, while demand is expected to revive, there are concerns over supply due to the ongoing stalemate between the UAE and the OPEC countries. According to the IEA, oil output from non-OPEC plus countries is set to rise in 2021. Given the projected demand of 96.4 mb/d in 2021, there could be an output gap this year, unless OPEC countries come to an agreement on increasing output.

Source : CNBC

Covid -19 Pandemic & The Economic Situation

While we do know how severely COVID-19 has affected public health and the global economy, the disease is a driver of global uncertainty and concern. While this kind of pandemic usually produces only a very short term economic impact, it can have some serious effects in particular areas of the economy. Because of the disease’s potential for further business disruption, the oil industry is concerned. If the outbreak is contained soon or turned into an endemic phase, we should be optimistic about how oil prices are going to respond but for now if the Delta variant continues to spread significantly globally, the demand for oil, and prices, will decline as travel and tourism are affected. For the oil business, that means a drop in jet fuel prices much greater than any decline in the price of gasoline.

Source : Gerson Lehrman Group (GLG)

Introduction of E-Mini WTI in CME

A factor to lookout for in the future in the introduction of the E-mini Crude oil futures contracts in July 2021 that are half the size of the full size WTI Crude Oil contract that consists of the West Texas Intermediate, (WTI) which has long been a benchmark for oil prices and has already traded over 50,000 contract since launching. This would allow traders to take advantage of the crude oil market with a lower margin requirement than the full size contract and its volatility, due to geopolitical, production and weather events allows traders to gain exposure in relatively straightforward manner compared to ETF counterparts. To add, trading in the e-mini contract will let traders to fine-tune their exposure and go short as easily as you can go long.

Source : Chicago Merchantile Exchange (CME) website

E-MINI CRUDE OIL FUTURES – CONTRACT SPECIFICATIONS

| CONTRACT UNIT | 500 barrels |

| PRICE QUOTATION | U.S. dollars and cents per barrel |

| TRADING HOURS | Sunday – Friday 6:00 p.m. – 5:00 p.m. (5:00 p.m. – 4:00 p.m. CT) with a 60-minute break each day beginning at 5:00 p.m. (4:00 p.m. CT) |

| MINIMUM PRICE FLUCTUATION | 0.025 per barrel = $12.50 |

| PRODUCT CODE | |

| CME Globex: QM | |

| CME ClearPort: QM | |

| Clearing: QM | |

| LISTED CONTRACTS | Monthly contracts listed for the current year and the next 5 calendar years. List monthly contracts for a new calendar year following the termination of trading in the December contract of the current year. |

| SETTLEMENT METHOD | Financially Settled |

| FLOATING PRICE | The Floating Price for each contract month will be equal to the Light Sweet Crude Oil Futures contract final settlement price for the corresponding contract month on the last trading day for the E-mini Crude Oil Futures contract month. |

| TERMINATION OF TRADING | Trading terminates 4 business days prior to the 25th calendar day of the month prior to the contract month (1 business day prior to the termination of trading in Light Sweet Crude Oil Futures). |

| SETTLEMENT PROCEDURES | E-mini Crude Oil Settlement Procedures |

| POSITION LIMITS | NYMEX Position Limits |

| EXCHANGE RULEBOOK | NYMEX 401 |

| BLOCK MINIMUM | Block Minimum Thresholds |

| PRICE LIMIT OR CIRCUIT | Price Limits |

Source : CME Website

A Short Term Price Outlook –

Source : Trading View

Given the uncertainty in demand caused by the ongoing pandemic and the capability of producers to increase output, there is unlikely to be a runaway rally towards $100 as yet. That said, oil-producing countries will be careful enough to maintain the balance in output so that prices do not crash either.

Prices will likely remain around $65 to $85 over the medium term. There is also no great geopolitical crisis brewing right now. If we look at the history of crude prices since 1950s, sharp spikes in prices were usually associated with geopolitical tensions between oil producing nations however the recent discussion among oil producing nations has resulted in an upwards momentum.

Download full article here

Disclaimer:

This document has been prepared solely for the use of the recipient. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means without the prior written permission from Kenanga Futures Sdn Bhd. Although care has been taken to ensure the accuracy of the information contained herein, Kenanga Futures Sdn Bhd does not warrant or represent expressly or impliedly as to the accuracy or completeness of the information. This information does not constitute financial or trading advice; neither does it make any recommendation regarding product(s) mentioned herein. Kenanga Futures Sdn Bhd does not accept any liability for any trading and financial decisions of the reader or third party on the basis of this information. All applicable laws, rules, and regulations, from local and foreign authorities, must be adhered to when accessing and trading on the respective markets.

Risk Disclosure:

Trading in contracts involves the risk of loss greater than your initial investment. This brief statement does not disclose all of the risks and other significant aspects of trading in contracts. In light of the risks, you should undertake such transactions only if you understand the nature of the contracts (and contractual relationships) into which you are entering and the extent of your exposure to risk. Trading in contracts is not suitable for many members of the public. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

For a full statement on risk disclosure, please refer to this link https://www.kenangafutures.com.my/wp-content/uploads/2020/09/RISK-DISCLOSURE-STATEMENT.pdf